PEO vs. Direct Benefits: What You Actually Gain (and Lose)

This isn’t a takedown of PEOs. They solve real problems for real companies. But understanding the trade-offs clearly is the only way to make a decision you won’t regret in eighteen months.

The decision to stay with a Professional Employer Organization or move to direct benefits administration rarely comes down to a single factor. It’s not about whether PEOs are “good” or “bad”—it’s about whether the trade-offs still make sense for your organization right now.

If you’re a growing company wrestling with this question, you’re not alone. Most HR leaders and CFOs at mid-sized companies hit a moment where they start wondering: Are we getting what we’re paying for? The answer requires looking honestly at what each model actually delivers—and what it costs you beyond the invoice.

What a PEO Actually Provides

A PEO enters into a co-employment arrangement with your company, becoming the employer of record for tax and benefits purposes while you maintain day-to-day control of your workforce. This structure allows smaller companies to access benefits typically reserved for larger employers, outsource compliance and payroll administration, and reduce the internal burden on lean HR teams.

For companies under 50 employees—especially those without dedicated HR staff—a PEO can be genuinely valuable. The bundled services reduce complexity, and the pooled buying power can mean better insurance rates than a small employer could negotiate independently.

The question isn’t whether PEOs provide value. It’s whether that value still outweighs what you’re giving up as your company grows.

The Control Question: Who’s Really Driving?

When you use a PEO, you’re renting someone else’s benefits infrastructure. That works fine until you want to make changes.

What You Gain with Direct Benefits

Plan design flexibility. With direct benefits, you choose your carriers, plan structures, contribution strategies, and voluntary benefits. Want to add a fertility benefit? Adjust your HSA contribution strategy? Offer a unique wellness program that reflects your company culture? Those decisions are yours to make.

Carrier relationships. Working directly with carriers (or through a broker you’ve selected) means you can negotiate, ask questions, and build relationships that serve your specific needs. You’re not limited to whatever the PEO has pre-negotiated across their entire book of business.

Timing control. Your renewal doesn’t have to align with the PEO’s master policy. You can time open enrollment, plan changes, and strategic decisions around what makes sense for your business—not someone else’s calendar.

What You Give Up Leaving a PEO

Administrative simplicity. Someone else was handling carrier relationships, compliance filings, COBRA administration, and the endless paperwork that comes with benefits. Now that’s on you (or your team, or vendors you hire).

Pooled buying power. Depending on your size and industry, you might lose access to rates you couldn’t get on your own. This varies significantly—some companies find comparable or better rates outside a PEO, while others see increases.

The “single throat to choke.” When everything is bundled, you have one vendor to call. With direct benefits, you’re coordinating between your HRIS, payroll provider, benefits broker, carriers, and various point solutions. That’s more relationships to manage.

The Transparency and Data Trade-Off

One of the most common frustrations with PEOs is the lack of visibility into what you’re actually paying for—and this extends to your own employee data.

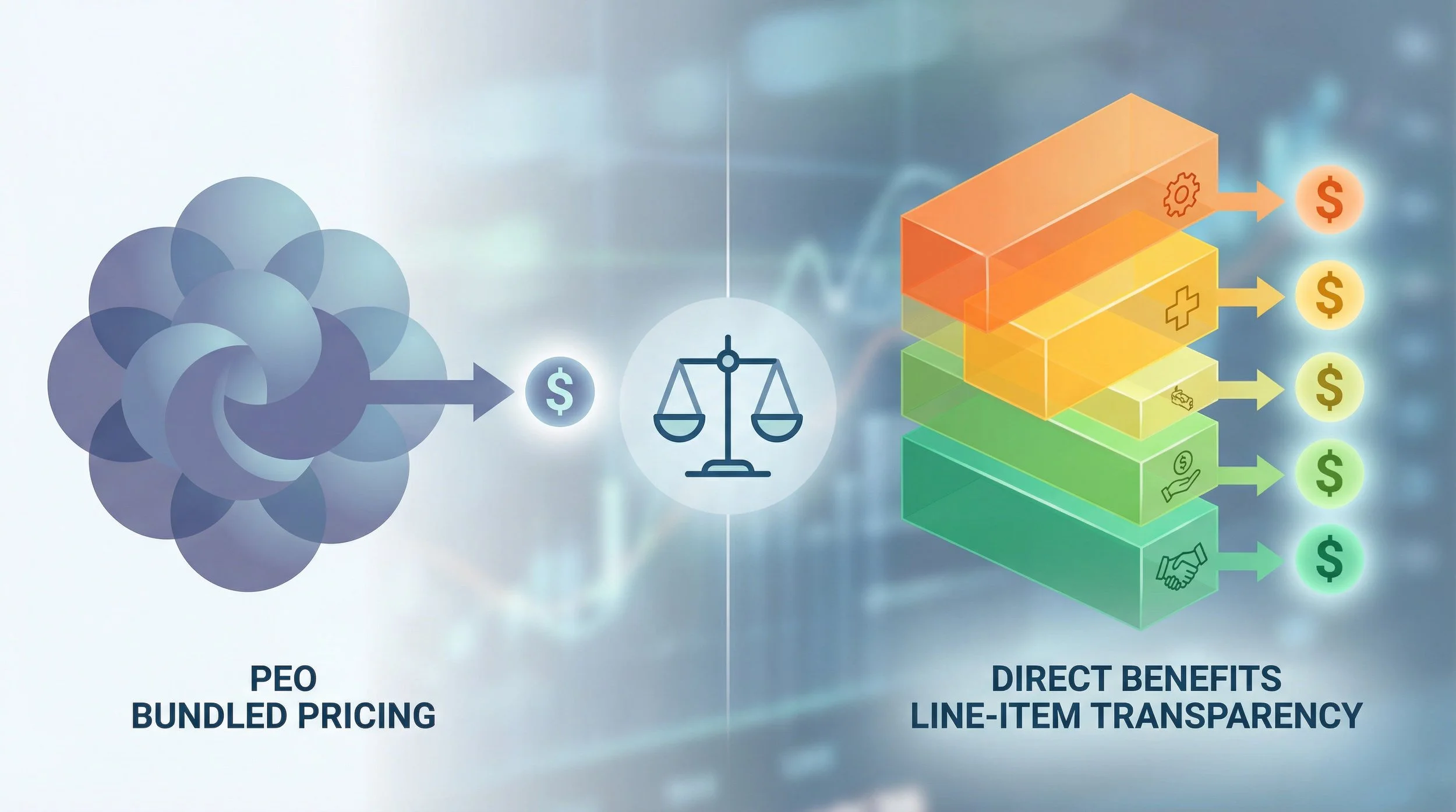

Direct benefits reveal line-item costs hidden in PEO bundled fee structures

What Direct Benefits Reveals

Line-item costs. When you administer benefits directly, you see exactly what you’re paying for each component—medical, dental, vision, life, disability, 401(k) administration, COBRA, and so on. No more bundled fees where it’s unclear how much is going to benefits versus administrative overhead.

Claims data access. With your own policies, you can often access claims data that helps you understand how your employees use benefits, identify cost drivers, and make informed decisions about plan design. Many PEOs restrict access to this data or provide it in limited formats.

Renewal transparency. When your broker presents renewal options, you can see the underwriting factors, compare multiple carriers, and understand exactly why rates are changing. PEO renewals often arrive as a single number with limited explanation.

Data Portability Matters

This catches companies off guard more often than it should. When you leave a PEO, you need your data—employee records, payroll history, benefits enrollment information, tax filings, and compliance documentation. How easily you can get that data varies significantly by PEO.

Before making a decision, ask your current PEO:

What data formats will be provided, and how long does export take?

Will historical payroll and tax records be accessible after termination?

What’s the timeline for final data delivery?

Are there fees associated with data export?

What You Lose Leaving

Simplicity in reporting. A single PEO report might cover everything—headcount, benefits enrollment, payroll costs, compliance status. With multiple vendors, you’re either building that consolidated view yourself or living with fragmented data.

Predictability (sometimes). Some PEOs offer rate guarantees or more stable pricing structures than the open market. If your company has had health events that would affect underwriting, staying in a larger risk pool might actually protect you.

The Plan Design Factor

This is where the conversation often gets real for growing companies.

With a PEO, you’re typically choosing from a menu of pre-selected plans. Those options might be good, but they’re designed to work across the PEO’s entire client base—not specifically for your workforce, industry, or culture.

What Direct Benefits Enables

Custom plan architecture. Maybe your workforce skews young and healthy, and a high-deductible health plan with robust HSA contributions makes more sense than traditional PPO options. Maybe you have an older population that values richer benefits. With direct plans, you design for your reality.

Voluntary benefits flexibility. Pet insurance, legal services, identity theft protection, student loan repayment—the voluntary benefits landscape has expanded significantly. Direct administration lets you curate offerings that match what your employees actually want.

Contribution strategy control. How you share costs between company and employees, how you tier family coverage, whether you incentivize certain plan choices—these decisions shape both your costs and your employees’ experience. Direct benefits puts those levers in your hands.

The Flip Side

Building this infrastructure takes time, expertise, and ongoing attention. If you don’t have the internal capacity or external partners to do it well, the flexibility becomes a burden rather than an advantage.

A Framework for Deciding

Rather than making this decision based on frustration with a recent renewal or excitement about theoretical flexibility, work through these questions systematically.

Cost Reality Check

What are you actually paying the PEO (total, including all fees)?

What would comparable services cost unbundled (benefits, payroll, HRIS, compliance)?

What’s the internal cost of managing multiple vendors?

Have you gotten actual quotes, or are you estimating?

Capacity Assessment

Do you have HR staff who can manage vendor relationships?

Who will handle open enrollment, compliance, employee questions?

What happens when your benefits person is on vacation or leaves?

Do you need to hire or contract additional support?

Strategic Fit

Does your current benefits program reflect your company’s values and culture?

Are there benefits you want to offer that your PEO can’t accommodate?

Is benefits strategy a competitive advantage you want to invest in?

How important is data access and transparency for decision-making?

Risk and Timing

How much complexity can your team absorb right now?

What’s your backup plan if the transition is harder than expected?

Are there business changes (M&A, rapid growth, market shifts) that affect timing?

The threshold varies by company. Some organizations thrive with a PEO at 200 employees; others hit friction at 50. Generally, a PEO might be outgrown once you’ve crossed 75–100+ employees, have HR capacity to manage vendors, are frustrated by opaque renewals or lack of plan flexibility, or need data access you can’t get. A PEO often remains the right choice for companies under 50 employees with limited HR bandwidth, those with challenging underwriting risk profiles, or businesses operating in multiple states that need compliance support they can’t build internally.

The Transition Reality

If you’re leaning toward leaving your PEO, understand that the transition itself is a project—one that requires planning and coordination. Most successful PEO exits take four to six months of preparation, with the actual transition often timed to coincide with benefits renewal dates and the start of a new calendar year to avoid mid-year payroll tax complications.

You’ll need to:

Source and select new vendors (broker, HRIS/payroll, benefits admin, retirement plan administrator)

Coordinate timing with your PEO contract and benefits renewal cycles

Migrate data from the PEO to your new systems

Communicate changes to employees clearly

Handle compliance requirements for state registrations, tax accounts, and benefits transitions

Rushing this process leads to problems—gaps in coverage, payroll issues, confused employees, compliance mistakes. If you can’t allocate the time and attention to do it right, it might be better to wait until you can.

Review your PEO contract carefully before committing to a timeline. Most contracts include termination provisions, but terms vary—some allow exit with notice, others include penalties or specific windows. Some companies negotiate exit terms as part of their initial PEO contract.

Making the Call

There’s no universal answer here. The right choice depends on your size, growth trajectory, internal capacity, industry, workforce needs, and strategic priorities.

What matters is making the decision based on actual trade-offs rather than assumptions. Get real quotes. Understand your current costs clearly. Assess your team’s capacity honestly. Think about what you need your benefits infrastructure to do—not just today, but in three years.

The companies that navigate this well are the ones that treat it as an infrastructure decision, not a vendor swap. They think about how benefits, HR technology, payroll, and compliance work together as a system. They plan before they execute.

And if the analysis says your PEO is still the right fit? That’s a legitimate answer. Staying put—with clear eyes about the trade-offs—is just as valid as leaving. If you’re wrestling with this decision and want a neutral perspective, Q Benefits Administration helps companies evaluate their options and plan transitions when the time is right. Book a consultation today.

Frequently Asked Questions

Will my benefits costs increase if I leave a PEO?

It depends on your company’s specific situation. Some organizations see cost reductions because they can design plans more efficiently for their workforce. Others—particularly those with health events or challenging risk profiles—may find that PEO pooling was protecting them from higher rates. The only way to know is to get actual quotes based on your employee census and claims history.

What internal resources do I need to manage benefits directly?

At minimum, you’ll need someone accountable for vendor relationships, open enrollment coordination, employee questions, and compliance monitoring. For companies under 150 employees, this is often part of an HR generalist’s role with broker support. Larger companies may need dedicated benefits staff.

About Q Benefits Administration

Q Benefits Administration is a benefits infrastructure consulting firm founded by Cora Lynn Alvar, SHRM-CP, a licensed Life and Health insurance professional with over a decade of experience in mid-market benefits and HR technology consulting. Q works with growing companies navigating complex benefits decisions—including PEO evaluations and transitions—providing impartial, project-based expertise. The firm’s approach emphasizes building internal capacity and creating structures that clients can own and maintain independently.

Works Cited

[1] National Association of Professional Employer Organizations — “What is a PEO?” https://www.napeo.org/what-is-a-peo

[2] Society for Human Resource Management — “PEOs: What HR Needs to Know.” https://www.shrm.org/topics-tools/news/benefits-compensation/peos-hr-needs-to-know