Have You Outgrown Your PEO? A Checklist for 75–500 Employee Employers

Your PEO relationship probably started out great. You got instant access to competitive benefits packages, someone handled the payroll headaches, and you had HR experts on call—all while you focused on growing your business. For a company under 50 employees, that bundled convenience often makes perfect sense.

But somewhere between your 75th and 150th employee, something shifted. The monthly invoices started including line items you don't quite understand. Your dedicated rep left, then their replacement left, and now you're explaining your business to someone new for the third time this year. When you asked for claims data to inform your benefits strategy, you hit a wall of "that's not how our system works."

If this sounds familiar, you're not alone. According to research from multiple benefits consulting firms, companies typically begin reconsidering their PEO relationship once they cross 50 employees[1][2], with the most common transition point falling between 75 and 100 employees[3]. At this stage, the model that once served you well can start constraining your growth instead of enabling it.

The question isn't whether PEOs are good or bad. It's whether yours still fits where your company is heading.

The Real Cost of Staying Too Long

Let's talk numbers first, because that's usually what prompts the initial "should we look at this?" conversation.

PEO fees typically run between $40 and $200 per employee per month[4][5], with most companies paying around $100 to $120[6]. For a company with 150 employees, that's $180,000 annually on the higher end of the range—before you factor in the actual cost of benefits, workers' compensation, and various pass-through charges.

But here's what most finance leaders miss in that calculation: the opportunity cost.

Last year, we worked with a 180-employee tech company that was paying $142 per employee monthly to their PEO—about $306,720 annually. When we ran the numbers on unbundling to a payroll provider, benefits broker, and HRIS platform, the total came to $187,000. That's $119,000 in annual savings, but the real story wasn't just the money.

They couldn't offer the mental health benefits their engineering candidates were asking about. They couldn't see their own claims data to understand what was driving costs, and they couldn't implement the performance management platform their leadership team wanted because it didn't integrate with the PEO's system.

The $119,000 was the easy part to measure. The strategic paralysis? That's harder to quantify until you're losing candidates to competitors with better benefits packages.

When Convenient Becomes Constraining: 15 Questions That Matter

Here's what we've learned after guiding dozens of companies through this evaluation: the decision to transition away from a PEO isn't just about cost or just about control. It's about whether the infrastructure you built for one stage of growth still serves the next one.

These 15 questions won't give you a points-based "score." They're designed to surface the conversations you need to have internally—and the ones you need to have with your PEO.

Cost & Financial Transparency

1. Can you itemize your total PEO costs without requesting a special report?

If you need to email your rep and wait for a breakdown of administrative fees, benefits costs, workers' comp premiums, and ancillary charges, that's your first red flag. You should be able to pull this information yourself, any day of the week[7].

One of the most common frustrations we hear from finance leaders is discovering that what looked like a straightforward monthly fee actually includes hidden markups on benefits premiums, mysterious "administrative adjustments," and per-transaction charges that only show up quarterly.

2. Have your per-employee costs increased faster than your headcount?

Some fee increases are expected as you add employees or when claims experience drives up insurance costs, but if your PEPM charges are climbing year over year without corresponding improvements in service or benefits, you're likely subsidizing higher-risk groups in the PEO's pool[8].

We've seen situations where a company's per-employee PEO cost jumped from $95 to $147 over two years despite zero high-cost claims and minimal headcount growth. When pressed, the PEO attributed it to "market conditions"—a non-answer that wouldn't fly in any other vendor relationship.

3. Could you rebuild these services independently at equal or lower cost?

This is where you need to do the actual math. What would it cost to:

Contract with a payroll provider like ADP, Paylocity, or Proliant ($25-50/employee/month)[9]

Work with a benefits broker (typically no direct cost—they're compensated through carrier commissions)

Implement an HRIS platform ($6-20/employee/month)[10][11]

Engage third-party administrators for COBRA, HSA/FSA ($3-8/employee/month)

Bring on fractional HR support for policy and compliance guidance ($50-150/hour as needed)

For many companies past 100 employees, the unbundled total comes in 20-30% lower than their PEO fees while providing significantly more flexibility[12].

Strategic Control & Customization

4. Do your benefits offerings match what your competitors are using to win candidates?

This is where the one-size-fits-all PEO model often breaks down first. If you're competing for product managers in a tight market and they're asking about fertility benefits, mental health coverage beyond EAP, or generous parental leave—can you offer that? Or are you limited to whatever's in the PEO's standard package?

Last quarter, a start-up SaaS company came to us specifically because they kept hearing "we went with the other offer because of the benefits package" in their exit interviews with final-stage candidates. Their PEO offered solid but generic coverage. The companies winning those candidates had customized their benefits to match their employer brand and employee demographics.

5. Can you implement your own HR policies, or are you working from PEO templates?

The template policy problem shows up in unexpected ways. We've worked with companies that wanted to offer:

Sabbatical programs after five years

Flexible parental leave beyond FMLA minimums

"Summer Fridays" or other schedule flexibility

Customized remote work policies for different roles

In each case, the PEO's response was some version of "our system doesn't support that" or "that's outside our standard framework." Your policies should reflect your company's values and culture, not your PEO's administrative convenience.

6. Can you select your own vendors for the HR tech you actually need?

This constraint hits hardest when you're trying to build an integrated HR tech stack. If you want to implement Lattice for performance management, BambooHR for employee records, or ChartHop for org planning—can you? Or are you locked into whatever limited platform your PEO provides?

The technology limitation becomes especially problematic if you're planning to scale quickly or if you're in a space where talent analytics and workforce planning are competitive advantages[13].

Data Access & Ownership

7. Do you have direct, unrestricted access to your claims data and utilization reports?

This is non-negotiable for strategic benefits management. You need to be able to pull reports showing health plan utilization, understand what's driving costs, identify trends, and use that data in renewal conversations with carriers.

If your PEO gatekeeps this information, charges extra for data exports, or provides it in formats that require translation, you don't really own your benefits program[14]. You're renting access to it.

8. Can you export clean employee data any time you need it—no fees, no waiting?

Your employee data belongs to you, period. If you need to run an equity audit, analyze compensation patterns, or prepare for a potential acquisition, you should be able to get complete, accurate data within minutes, not days[15].

We've seen PEOs charge "administrative fees" ranging from $500 to $5,000 for data exports. We've also seen situations where companies gave notice of their intent to leave and suddenly found their data export requests stuck in mysterious delays for weeks.

9. Do you have access to your complete historical records without restrictions?

This becomes critical when you eventually transition. You'll need W-2s, benefits enrollment records, workers' comp claim history, and COBRA documentation. Companies that wait until they've given notice to request historical records often discover incomplete files, missing documentation, or significant gaps in record-keeping[16].

Service Quality & Partnership

10. Do you have a consistent point of contact who knows your business?

High rep turnover is one of the clearest signs that your PEO is struggling with either internal operational issues or a business model that doesn't prioritize relationship continuity. If you're re-explaining your company's structure, benefits philosophy, and current projects every six months, you're not getting the strategic HR partnership you're paying for[17].

11. When you have an urgent question, how long do you actually wait for answers?

We ask companies to think about their last three urgent requests—maybe a same-day payroll correction, a time-sensitive compliance question, or an employee who needs immediate help with a benefits issue. How long did resolution take?

If you're sitting in ticket queues for 24-48 hours on urgent matters, the "convenience" of PEO outsourcing is creating more stress than it's eliminating. Companies that have transitioned often tell us the biggest surprise was how much more responsive their unbundled vendors are compared to their PEO's shared service model.

12. Does your PEO proactively bring you compliance updates and strategic guidance?

There's a difference between a PEO that sends you generic compliance alerts and one that reaches out proactively to say "here's a new regulation that affects your California employees specifically, and here's what we recommend you do about it."

Strong PEOs add value by translating regulatory complexity into actionable guidance. If yours is reactive—or worse, if you're learning about compliance requirements from sources other than your PEO—you're not getting the expertise you're paying for[18].

Growth Trajectory & Strategic Fit

13. Will your PEO support your growth plans for the next three years?

If you're planning to double your headcount, expand into new states, shift to a remote-first model, or scale internationally, you need to know whether your PEO can grow with you. Some PEOs serve small companies beautifully but don't have the infrastructure or expertise to support rapid scaling or geographic expansion[19].

An example of this would be a SaaS company with 120 employees and receives funding to scale to 300+ in 18 months. Their PEO contract will likely require a renegotiated contract at 150 employees with no guarantee of continued service. Rather than risk a forced mid-year transition during their growth phase, a pre-emptive strategic exit allows the company to build the benefits infrastructure to scale with them.

14. Do your leadership team and board have confidence in your HR infrastructure?

This is the qualitative question that matters more than most people admit. If your CEO is asking uncomfortable questions about cost transparency, your CFO wants better financial reporting, or your board is raising concerns about data access and strategic control, those conversations won't disappear. They'll intensify.

And if you're approaching a fundraising round or potential acquisition, having clearly defined HR infrastructure with accessible data becomes a diligence requirement, not a nice-to-have.

15. If you were building your HR infrastructure from scratch today, would you choose a PEO?

Strip away sunk costs and the switching anxiety. If you were standing at your current size and trajectory and designing your HR infrastructure now, would a PEO be the right answer?

Sometimes the answer is still yes—maybe you're experiencing temporary but intense growth and need the bundled convenience for another year. But often, the answer is "probably not," and that tells you what you need to know.

What Your Answers Are Telling You

If you answered "no" or "I'm not sure" to five or more questions—particularly in the cost, control, or data access categories—you've likely outgrown your PEO model. That doesn't mean you need to exit tomorrow, but it does mean you should start planning.

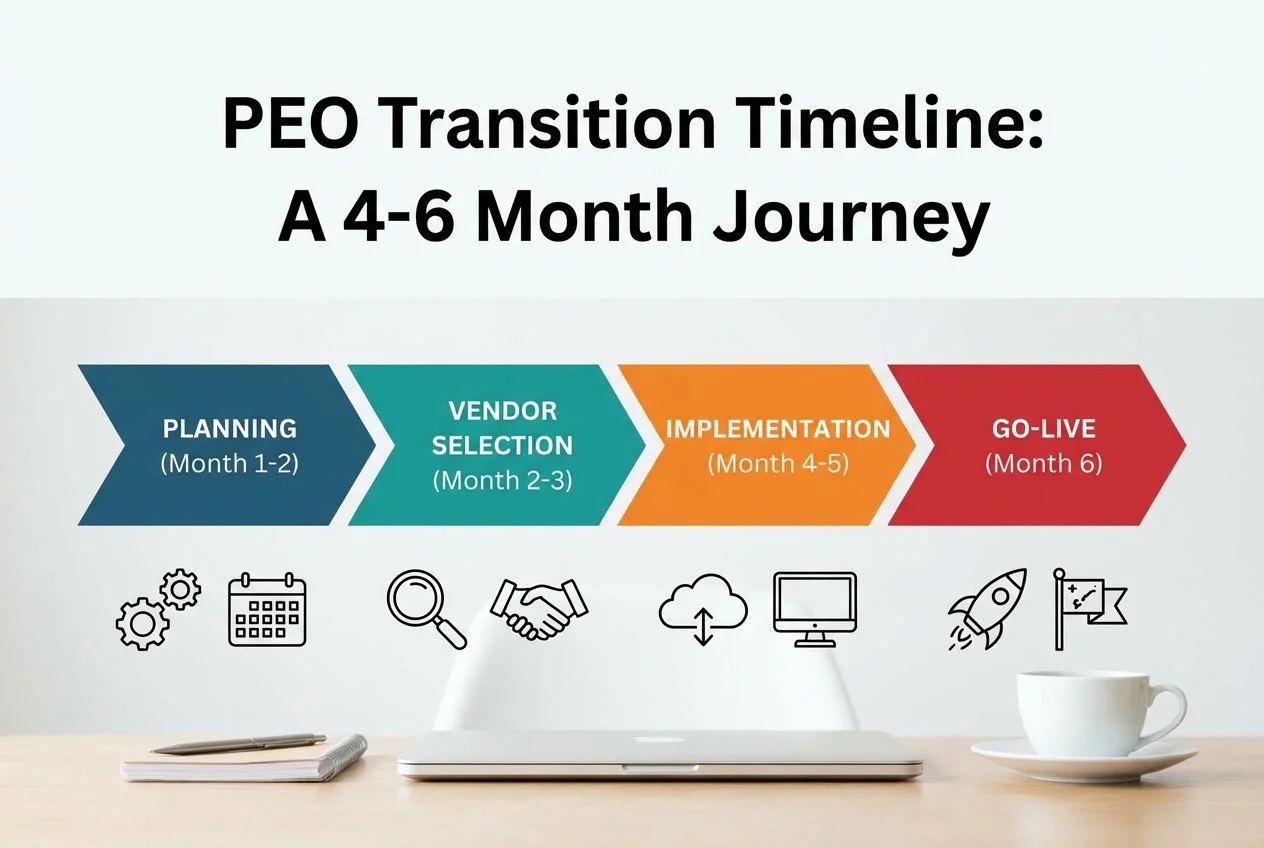

The companies that handle PEO transitions most successfully are the ones who approach it as a strategic project rather than a reactive scramble. In our experience working with mid-sized companies on these transitions, the timeline looks something like this:

Months 1-2: Assessment and decision

Run the financial analysis comparing PEO costs to unbundled alternatives

Evaluate your current pain points and strategic constraints

Review your PEO contract for notice periods, termination fees, and renewal dates

Build internal consensus around the decision

Months 3-4: Vendor selection

RFP process for benefits broker

Assessment of retirement plan providers

HRIS platform evaluation and selection

Payroll provider comparison

TPA selection for COBRA, HSA/FSA, and other ancillary services

Months 5-6: Implementation and transition

HRIS implementation and data migration

Benefits broker market analysis and carrier selection

Retirement plan setup

Payroll system setup and testing

Employee communication campaign

Go-live and post-transition support

Most sources recommend a minimum of three to six months for PEO transitions[20][21], but we typically advise six to nine months depending on your PEO contract. The extra time eliminates the rushed decisions and midnight fire drills that can derail transitions.

The Timing Question Everyone Asks

"When should we actually do this?"

The ideal transition timing aligns with three factors:

Your benefits plan year. If you can exit your PEO effective December 31st and align with a January 1st benefits renewal, you'll avoid the complexity of resetting deductibles mid-year and managing two open enrollment periods in the same 12-month span[22].

Calendar year-end. Transitioning at year-end avoids the tax wage-base reset problem for SUTA, FICA, and FUTA that can create double-taxation scenarios in mid-year exits[23][24]. While there are ways to manage mid-year transitions, year-end is cleaner.

Your team's bandwidth. Don't attempt a PEO transition during your busiest season or while you're managing other major initiatives. You need dedicated project management attention to coordinate data migration, vendor onboarding, and employee communications.

If you can't hit year-end timing, early Q1 is often the second-best option. You get clean W-2s from your PEO for the previous year, and you have most of the year to stabilize before the next benefits renewal cycle.

What Comes After: The Unbundled Model

One of the biggest misconceptions about leaving a PEO is that you need to build a massive internal HR department. You don't.

The modern alternative looks more like this:

Payroll provider – Handles tax filing, direct deposits, garnishments, and compliance automation. Most mid-sized companies spend $25-50 per employee monthly[25].

Benefits broker – Acts as your fiduciary advisor, runs carrier RFPs, negotiates on your behalf, and provides strategic benefits consulting. Typically compensated through carrier commissions rather than direct fees.

HRIS platform – Serves as your system of record for employee data, onboarding, time tracking, PTO management, and reporting. Costs range from $6-20 per employee monthly depending on features[26].

Third-party administrators – Handle specialized functions like COBRA administration, HSA/FSA management, and retirement plan services. Usually $3-8 per employee monthly.

HR consultant or fractional HR – Provides expertise on policy development, compliance guidance, and strategic HR projects. Typically $150 to $250/hour, depending on services, regularity, and geographic location. Engage as needed rather than as a fixed cost.

The critical difference: you control each vendor relationship, you own all your data, and you can swap out any piece that's not working. It's infrastructure, not vendor lock-in.

How Q Benefits Administration Approaches PEO Transitions

Here's where we acknowledge the obvious: we're writing this article because helping companies navigate these decisions is what we do. But we do it differently than most.

We're not a PEO and we're not a vendor of HR software. That's intentional. We're an independent benefits infrastructure consultancy, which means our only product is expertise—project-based, impartial guidance that helps you make decisions without forcing solutions we profit from.

When a company comes to us evaluating whether to leave their PEO, we start with the same analysis we've shared here. Sometimes we conclude that staying makes sense for another year or two. More often, we help companies design and implement the unbundled infrastructure that fits their stage and strategy.

That work typically involves:

Running the cost analysis and building the business case you can take to leadership

Coordinating the RFP process for brokers, HRIS platforms, and other vendors

Project-managing the entire transition so nothing falls through the cracks

Building governance structures and documentation your internal team can own going forward

Serving as the neutral party who keeps vendors honest and focused on your interests, not theirs

The companies that work with us typically tell us the same thing afterward: "I didn't realize how much we didn't know we didn't know." Benefits infrastructure has its own language, its own hidden complexity, and its own cast of vendors who all believe their solution is the answer to everything. Having someone who's guided dozens of companies through this exact process—and who isn't selling you anything but advice—makes the difference between a smooth transition and a chaotic one.

Having The Conversation With Leadership

If you're the HR or finance leader who needs to walk into the CFO's office or the next board meeting and raise the "have we outgrown our PEO?" question, here's how to frame it:

"I've been evaluating our HR infrastructure, and I want to share some findings. Our PEO served us well when we were smaller, but at [X] employees, we're seeing misalignment in three critical areas: cost transparency, strategic flexibility, and data ownership. I've put together a comparison of what it would cost to unbundle these services versus staying with our current provider, and I'd like to discuss whether a transition makes sense in the next 6 to 12 months."

Then walk through the specific pain points where you answered "no" on the checklist—the lack of claims data that's preventing you from managing benefits costs strategically, the inability to offer competitive benefits that's costing you candidates, or the monthly fees that now exceed what you'd pay for best-in-class unbundled services.

Leadership doesn't need to understand COBRA administration or SUTA tax accounts. They need to understand the business impact: that your current setup is either costing more than it should, limiting your ability to compete for talent, or creating unnecessary risk.

The Bottom Line

Outgrowing your PEO isn't a failure—it's a milestone. It means your company has evolved past the stage where a bundled HR outsourcing model serves you well.

The question isn't whether you'll eventually need to make a change. Most companies in the 75-500 employee range do. The question is whether you'll plan that change strategically or scramble reactively when something breaks.

If this checklist surfaced more concerns than confirmations, it's time to have the conversation. And if you want a neutral second opinion on your specific situation—one that doesn't come from someone trying to sell you their PEO, their brokerage services, or their software platform—we can help with that.

Ready to evaluate your options? Request a consultation with Q Benefits Administration to discuss your PEO transition strategy.

Frequently Asked Questions

How long does a PEO transition typically take?

Most PEO transitions require between six and 12 months from decision to go-live[27][28]. The timeline depends on several factors: the complexity of your benefits structure, the number of employees, how many states you operate in, and whether you're aligning the transition with your benefits renewal or calendar year-end. Companies that rush the process—trying to exit in 30-60 days—often encounter problems with data migration, employee communications, or coverage gaps. We typically recommend four to eight months if you have that flexibility, which allows time for thoughtful vendor selection, proper employee communication, and contingency planning.

What are the biggest risks of leaving a PEO mid-year?

The primary risk is tax wage-base resets for FICA, FUTA, and SUTA taxes[29][30]. When you leave a PEO mid-year, your employees' wage bases may reset to zero under your company's new tax ID number, which can result in double-taxation on wages already earned. Additionally, employees who have met their health insurance deductibles or out-of-pocket maximums may have to start over at zero under new plans, increasing their healthcare costs. There's also complexity around COBRA participants, workers' compensation coverage continuity, and FSA balance transfers. While mid-year exits can be managed successfully, they require longer and more careful planning.

Can we negotiate better terms with our current PEO instead of leaving?

Possibly, but with important caveats. PEOs typically have limited flexibility on their core service model and administrative fees because they're built on pooled structures with standardized processes. However, if you're a larger account (100+ employees), you may have leverage to negotiate improved service level agreements, better cost transparency, or adjusted fee structures. Before your renewal, we recommend running a parallel process—get quotes from benefits brokers and HRIS vendors to understand what you'd pay in the open market. This gives you concrete data for negotiations and ensures you're making an informed decision rather than accepting renewal terms out of inertia or fear of change.

What happens to our employees' benefits during the transition?

With proper planning, employees should experience minimal disruption. The key is coordinating timing so health, dental, and vision coverage continues without gaps—typically by aligning the switch with open enrollment or plan year changes. There is typically a 30-60 day “black-out” period for Retirement Plan assets transfer to your new 401(k) provider (employees usually don't need to take action), FSA and HSA accounts move to new administrators, and life insurance plus disability coverage shifts to new carriers[31][32]. The most important element is clear, proactive communication. Employees need to understand what's changing, what's staying the same, when changes take effect, and who to contact with questions. Companies that handle transitions well typically host Q&A sessions, send regular email updates, and provide side-by-side benefit comparisons 60-90 days before the switch.

How much does it actually cost to leave a PEO and set up independent infrastructure?

Setup costs vary based on company size and needs. Initial expenses typically include PEO contract termination fees (if you're exiting before your contract term ends), HRIS implementation costs ($5,000-$15,000 for most mid-sized companies)[33], benefits broker setup (usually no charge), and potentially consulting support to manage the transition. Ongoing costs include payroll provider fees ($25-50/employee/month), HRIS subscription ($5-20/employee/month)[34], TPA fees for COBRA and other services ($3-8/employee/month), and possibly fractional HR support for specialized projects. For companies with 100+ employees, the total unbundled cost often equals or falls below PEO fees while providing significantly more control and transparency. The actual ROI isn't just cost savings—it's the strategic capabilities you gain around data access, benefits customization, and technology selection.

Expert Perspective & Credentials

About Q Benefits Administration

This analysis reflects Q Benefits Administration's direct experience specializing in benefits infrastructure consulting for organizations in the 75-500 employee range—the exact inflection point where PEO relationships most commonly require reassessment.

Unlike PEO providers or HR technology vendors, Q Benefits Administration is an agnostic independent consultancy. Although vendors may pay referral fees, Q ensures all clients are presented with suitable options, whether or not that vendor pays a referral fee.

Founder Expertise:

Q Benefits Administration was founded by Cora Lynn Alvar, SHRM-CP, who has over a decade of experience in health and welfare benefits consulting, retirement plan services, and HR infrastructure design for mid-market organizations. Prior to founding Q Benefits, Cora Lynn worked with large national brokerages managing complex benefits programs and benefits-technology transition projects for companies across multiple industries.

Why We Wrote This

This article synthesizes insights from our client engagements, industry research, and direct conversations with HR and finance leaders at dozens of mid-sized companies. We wrote it because we kept having the same conversation repeatedly: smart, capable leaders who knew something wasn't working with their PEO but weren't sure if they were just being difficult or if their concerns were valid. They needed a framework for evaluation that didn't come from someone trying to sell them something.

Our Perspective on PEOs

We're not anti-PEO. For companies under 50 employees, particularly fast-growing startups that need to focus on product and market fit rather than HR infrastructure, PEOs can be excellent solutions. But we've seen too many companies stay in PEO relationships past the point where they make strategic sense—simply because no one gave them permission to ask whether there was a better way.

Disclaimer

This article provides general educational information about PEO transitions and benefits infrastructure for small and mid-sized employers. It is not intended as legal, tax, accounting, or financial advice, and should not be relied upon as such.

Every company's situation is unique, and PEO contracts vary significantly in their terms, fees, and termination provisions. Before making any decisions about terminating or modifying a PEO relationship, consult with qualified legal, tax, and HR professionals who can assess your specific circumstances, review your actual contract terms, and advise on compliance obligations specific to your industry and jurisdictions.

The cost figures, timelines, and recommendations in this article are based on industry averages and Q Benefits Administration's client experience as of November 2025. Your actual costs and timelines may differ based on company size, location, industry, benefits complexity, and current market conditions.