Do You Actually Need a PEO? A Decision Guide for Seed-Stage Founders

Audio Overview

You just closed your seed round. The bank account looks healthier than it ever has. Now someone—maybe your lawyer, maybe your first advisor, maybe that founder friend two years ahead of you—has dropped the acronym: PEO.

HR Manager Wondering if Her Seed-Stage Startup Needs a PEO

Professional Employer Organization. It sounds official. It sounds like something a real company would have. The question nobody seems to answer clearly: do you actually need a PEO right now, or is it overkill for a team of seven people working out of a WeWork?

The honest answer is frustrating: it depends. “It depends” doesn’t help you make a decision before your first hires start asking about health insurance. Let’s break this down into something actually useful—a framework for thinking through whether a PEO makes sense at this exact moment, or whether another path gets you where you need to go.

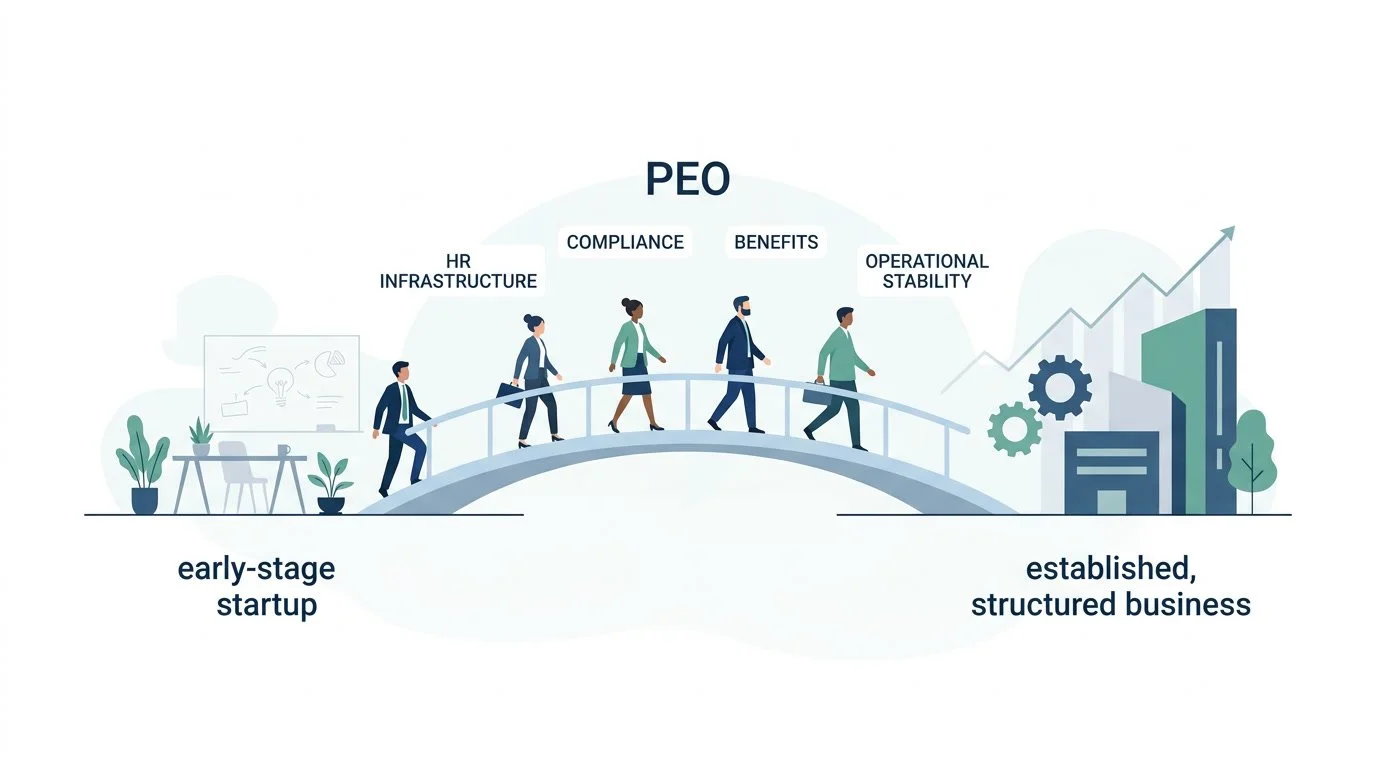

What a PEO Actually Does (and Doesn’t Do)

A PEO is a co-employment arrangement. You remain the worksite employer—you manage your people, set salaries, decide who gets hired and fired—while the PEO becomes the employer of record for tax and benefits purposes [1]. That means they handle payroll processing, benefits administration, employment tax filings, and often workers’ compensation insurance. More than 230,000 U.S. businesses currently partner with a PEO, and nearly two-thirds of those clients have between 10 and 49 employees [2].

The pitch is compelling: access to big-company benefits at small-company scale, compliance support across multiple states, and one vendor handling the HR infrastructure you don’t have time to build. What a PEO doesn’t do is replace your need for HR strategy (they administer, they don’t advise on your people philosophy), give you unlimited flexibility (you’re often limited to their carrier options and plan designs), or scale infinitely with you. Many companies outgrow their PEO within three to five years, and the exit can be complex [3].

That distinction matters because the decision isn’t really “PEO vs. no PEO.” It’s “PEO vs. other ways of solving the same problems.”

The Three Paths for Seed-Stage Benefits Infrastructure

Path 1: Join a PEO. Outsource payroll, benefits, and compliance to a bundled provider. Setup takes two to four weeks, and you get immediate access to group health plans that would otherwise require more employees to qualify for. Best for founders moving fast with limited HR experience and multi-state hiring plans. Trade-offs: less control over plan design, potential for opaque pricing, and eventual transition complexity.

Path 2: Build It Yourself. Set up your own payroll (Gusto, Rippling, or similar), work with an insurance broker for health coverage, and handle compliance state by state. Best for founders with some HR experience, companies concentrated in one or two states, and those who want maximum control from day one. Trade-offs: more administrative burden, steeper learning curve, and responsibility for every jurisdiction where you have employees.

Path 3: Hire HR Early. Bring on a dedicated HR person or fractional HR support to build the infrastructure with your input. Best for founders who see people operations as strategic, companies with complex hiring needs, and those who want a human being accountable for the function. Trade-offs: adds headcount cost early and requires finding someone who operates at both strategic and tactical levels.

Most guides won’t tell you: these paths aren’t mutually exclusive. A PEO can serve as a temporary bridge while you figure out your longer-term infrastructure plan.

The Founder Decision Framework: 10 Questions

Instead of a vague “consider your needs” recommendation, here’s a practical scoring model. Answer each question honestly, assign the listed points, and tally your total.

Scoring Your Results

22–30 points: PEO is likely your best path. You’re moving fast, wearing too many hats, and need competitive benefits without building infrastructure from scratch. A PEO will buy you 12–24 months of breathing room.

14–21 points: Either path could work. You have reasons to consider a PEO and reasons to build it yourself. Consider what you value more: control and customization (lean DIY) or speed and simplicity (lean PEO). A fractional HR consultant could help you think through this tradeoff.

7–13 points: DIY or early HR hire fits better. You have the bandwidth, expertise, or strategic priority to build your own benefits infrastructure. Just make sure you’re allocating real time to do it right.

0–6 points: Hire HR help now. You have strong preferences, significant complexity, or enough scale that in-house management makes sense—with dedicated support. Consider a fractional HR leader or a full-time hire with benefits experience.

The Temporary PEO Strategy: A Bridge, Not a Destination

Strategic use of a PEO for startups as an intentional temporary benefits solution

Here’s a perspective that doesn’t get enough airtime: a PEO can be an intentional temporary solution. Too many founders treat PEO vs. DIY as a permanent choice. The smart play is often to use a PEO for the first 18–24 months while building product-market fit, then plan a deliberate transition when you hit certain milestones.

This works when you know from the start you’ll likely outgrow the arrangement, document what you’re learning along the way, set a trigger point for reassessment (headcount milestone, funding round, renewal date), and budget time for the eventual transition. Pay attention to renewal cycles—most PEO contracts auto-renew, and breaking mid-cycle can be complex. Start exit planning at least six months before you want to make the switch [3].

Before signing, ask three questions that separate good PEO partners from problematic ones: What’s included in the per-employee fee and what costs extra? Can you use your own HRIS for certain functions, or must you use their platform exclusively? What’s the typical timeline and process for clients who transition off? Vendors who answer clearly and without defensiveness are worth working with.

Think of the PEO as scaffolding. It supports the structure while you’re building. Eventually, the building needs to stand on its own.

When to Revisit This Decision

Whatever path you choose, set a calendar reminder at these milestones: headcount doubles, you raise your next round, your first benefits renewal arrives (you’ll finally have real cost data), you expand to three or more states, or a key employee raises concerns about your benefits setup. Your needs at 8 employees are different from your needs at 25, which are different from your needs at 75. The goal isn’t a permanent decision today—it’s the right decision for right now, with a clear view of when you’ll reassess.

Making the Call

There’s no universally correct answer to whether a seed-stage startup needs a PEO. The right answer depends on your team’s experience, your hiring plans, your risk tolerance, and—honestly—how much you enjoy thinking about health insurance. What matters is making a deliberate choice rather than a default one. Use the framework, score yourself honestly, and remember that this is an infrastructure decision, not a one-way door.

Frequently Asked Questions

Can I leave a PEO whenever I want?

Technically yes, but practically it’s more complicated. Most PEO contracts have specific notice requirements aligned with benefit plan years. Leaving mid-year can create coverage gaps and complicate payroll tax filings. Plan your exit around renewal cycles, and start the process at least 90–180 days before your target transition date [3].

Is a PEO more expensive than doing it myself?

It depends on scale. PEOs charge administrative fees but often provide access to better benefits pricing than very small employers can secure independently. The math changes as you grow—many companies find they achieve better economics once they reach 50–75 employees and can negotiate directly with carriers [4].

Do I lose control of my employees if I join a PEO?

No. The co-employment model means the PEO handles administrative functions, while you remain responsible for day-to-day management, hiring, firing, compensation decisions, and work assignments. You’re still the boss; they’re handling paperwork [1].

What’s your Q? If you’re wrestling with this decision and want a thought partner who’s seen the PEO question from every angle, we’re here to help you think it through—no commitment, no pressure, just clarity. Bring us your Q.

About Q Benefits Administration

Q Benefits Administration helps seed-stage and growth-stage companies make smarter decisions about benefits infrastructure—whether that means evaluating a PEO, planning a transition to in-house administration, or building your HR tech stack from scratch. Founded by Cora Lynn Alvar (SHRM-CP), a licensed Life & Health insurance agent with over a decade of experience in mid-market benefits consulting, Q brings deep expertise in PEO relationships, benefits strategy, and HR technology selection. When clients need policy placement, QBA Insurance Solutions can help implement the right coverage. Our approach is advisory-first: we help you see the full picture so you can make decisions that serve your company’s long-term interests.

Cited Works

[1] NAPEO — “What is a PEO?” https://www.napeo.org/what-is-a-peo. Accessed: 2026-02-26.

[2] NAPEO — “PEO Clients: An Analysis.” https://napeo.org/wp-content/uploads/2025/03/2024-white-paper-final.pdf. Published: 2024. Accessed: 2026-02-26.

[3] SHRM — “PEOs: Pros and Cons for Employers.” https://www.shrm.org/topics-tools/news/benefits/peos-pros-cons-employers. Accessed: 2026-02-26.

[4] NAPEO — “Industry Overview.” https://napeo.org/intro-to-peos/industry-overview/. Accessed: 2026-02-26.