Renewal Fatigue Is Real: How to Stop Re-Living the Same Chaos Every Year

Every year, the same story unfolds. Underwriting results land in your inbox with little warning. Leadership wants answers you don't have yet. Employees hear rumors about rate increases. Decisions that should take weeks get crammed into days.

Renewal fatigue is real—and it's not a personal failing. It's a systems problem.

If open enrollment season feels like controlled chaos (emphasis on chaos), you're not alone. Most HR and finance leaders experience this annual cycle of scrambling, reacting and white-knuckling through decisions that affect every employee in the organization. The exhaustion compounds year after year because nothing structurally changes between renewals.

Here's the good news: renewal fatigue is fixable. Not with heroic effort during crunch time, but with a planning system that distributes the work across the entire year. Planning is the antidote to chaos—and once you have a system, you stop re-living the same fire drill every twelve months.

Why Renewal Season Feels So Chaotic

Before building a better system, it helps to understand why the current one breaks down.

Compressed timelines create pressure cookers. Most employers receive renewal information 60–90 days before their plan year begins [1]. That window sounds reasonable until you factor in broker negotiations, leadership approvals, employee communication, enrollment system updates and vendor coordination. Suddenly, eight weeks feels like eight minutes.

Reactive decision-making replaces strategy. When underwriting results drive the conversation, you're negotiating from a defensive position. Rate increases become the story instead of benefit value, employee experience or competitive positioning. Leadership asks "how do we minimize this?" rather than "does this program still fit our strategy?"

Stakeholder alignment happens too late. Finance hears about benefits costs when there's no time to adjust budgets. Department heads learn about plan changes days before open enrollment. Employees get confused by rushed communications. Everyone feels blindsided because they were blindsided.

Institutional knowledge disappears. Without documentation, each renewal starts from scratch. Why did you choose that carrier three years ago? What was the employee feedback on the HSA rollout? Which broker promises never materialized? These answers live in scattered emails—or nowhere at all.

The pattern repeats because nothing interrupts it. Same timeline, same scramble, same exhaustion.

Planning as the Antidote to Renewal Chaos

The organizations that experience calm renewal seasons don't have easier circumstances. They have better systems.

Planning transforms renewal from a 60-day crisis into a 12-month process. Work distributes across the calendar. Stakeholders engage early. Decisions get made with context instead of panic. The actual renewal window becomes execution of a plan rather than creation of one.

This isn't about adding more work—it's about moving work to better timing. The same conversations happen either way. The question is whether those conversations happen under duress or with breathing room.

Consider the difference:

Reactive approach: Renewal results arrive. You schedule emergency meetings. Finance pushes back on costs. You scramble to model alternatives. Leadership picks the least-bad option. Employees get two weeks to understand changes and make elections.

Planned approach: Six months before renewal, you review the current program against organizational priorities. Four months out, you establish budget parameters with finance. Two months out, when renewal results arrive, you already know your negotiating position and have pre-approved alternatives ready. Employees get clear, timely communication because you planned for it.

Same amount of effort. Radically different experience.

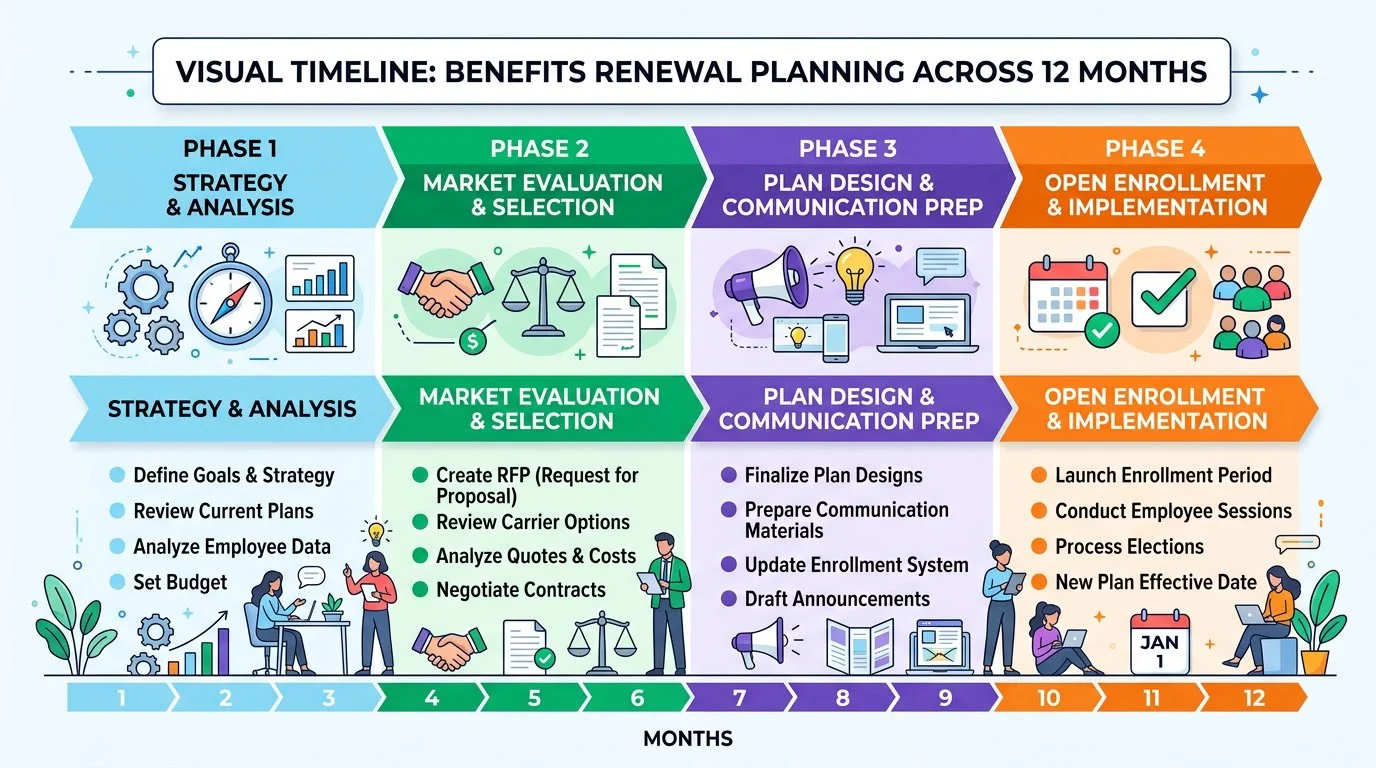

The 12-Month Renewal Calendar

Benefits renewal planning distributes work across the year to eliminate chaos

A functional renewal calendar breaks the year into four phases. Each phase has specific objectives, and work in one phase sets up success in the next.

Phase 1: Post-Renewal Review (Months 1–3 After Plan Year Begins)

This phase gets skipped most often—and that's exactly why chaos repeats. Right after open enrollment, everyone wants to forget about benefits for a while. Resist that impulse.

Objectives:

Document what worked and what didn't during the last renewal

Capture employee questions, complaints and feedback

Note any vendor or broker performance issues while they're fresh

Archive key documents and decision rationale for future reference

Key activities:

Conduct a 30-minute debrief with anyone involved in renewal

Survey employees about enrollment experience and benefit understanding

Create a "lessons learned" document that lives somewhere findable

Update your benefits inventory (what you offer, who administers it, contract end dates)

This phase takes minimal time but creates massive leverage. When you sit down for the next renewal, you'll have context instead of guesswork.

Phase 2: Strategic Assessment (Months 4–6)

Mid-year is the right time to ask fundamental questions about your benefits program. Far enough from the last renewal to have perspective. Far enough from the next one to actually make changes.

Objectives:

Evaluate program alignment with organizational strategy and values

Identify coverage gaps or redundancies

Assess vendor and broker performance against commitments

Surface any compliance concerns early

Key activities:

Review benefits benchmarking data for your industry and geography [2]

Compare current offerings against employee demographics and feedback

Evaluate broker relationship: Are they proactive? Do they bring ideas?

Check plan documents and required notices for compliance gaps

Identify any benefits you're paying for that employees don't use

This phase often reveals that renewal chaos stems from upstream problems: wrong broker fit, misaligned plan design or benefits that made sense five years ago but don't match your current workforce.

Phase 3: Pre-Renewal Preparation (Months 7–9)

This is where most organizations start their renewal process—but in a planned approach, you're arriving with homework already done.

Objectives:

Establish budget parameters and approval thresholds with leadership

Define negotiating priorities and walk-away points

Prepare alternative scenarios before you need them

Align stakeholders on timeline and decision-making process

Key activities:

Meet with finance to discuss benefits budget expectations

Create a renewal brief for leadership: current state, priorities, constraints

Develop 2–3 alternative benefit designs (richer, leaner, restructured)

Confirm broker timeline for renewal marketing

Draft preliminary employee communication timeline

The magic here is having options before you see underwriting results. If rates come in high, you already have modeled alternatives. If they come in favorable, you can propose enhancements you've already vetted.

Phase 4: Renewal Execution (Months 10–12)

With three phases of preparation behind you, the actual renewal window becomes tactical execution rather than strategic scrambling.

Objectives:

Negotiate renewal terms from a position of knowledge

Make final decisions aligned with pre-established criteria

Execute employee communication and enrollment

Document decisions for the next cycle

Key activities:

Review renewal results against prepared scenarios

Negotiate with carriers using benchmarking data and alternative quotes

Present recommendations to leadership with clear rationale

Communicate changes to employees with adequate lead time

Run enrollment process with support resources ready

Begin documenting for next year's Phase 1

When you reach this phase prepared, the stress doesn't disappear entirely—but it becomes manageable. You're executing a plan, not inventing one under pressure.

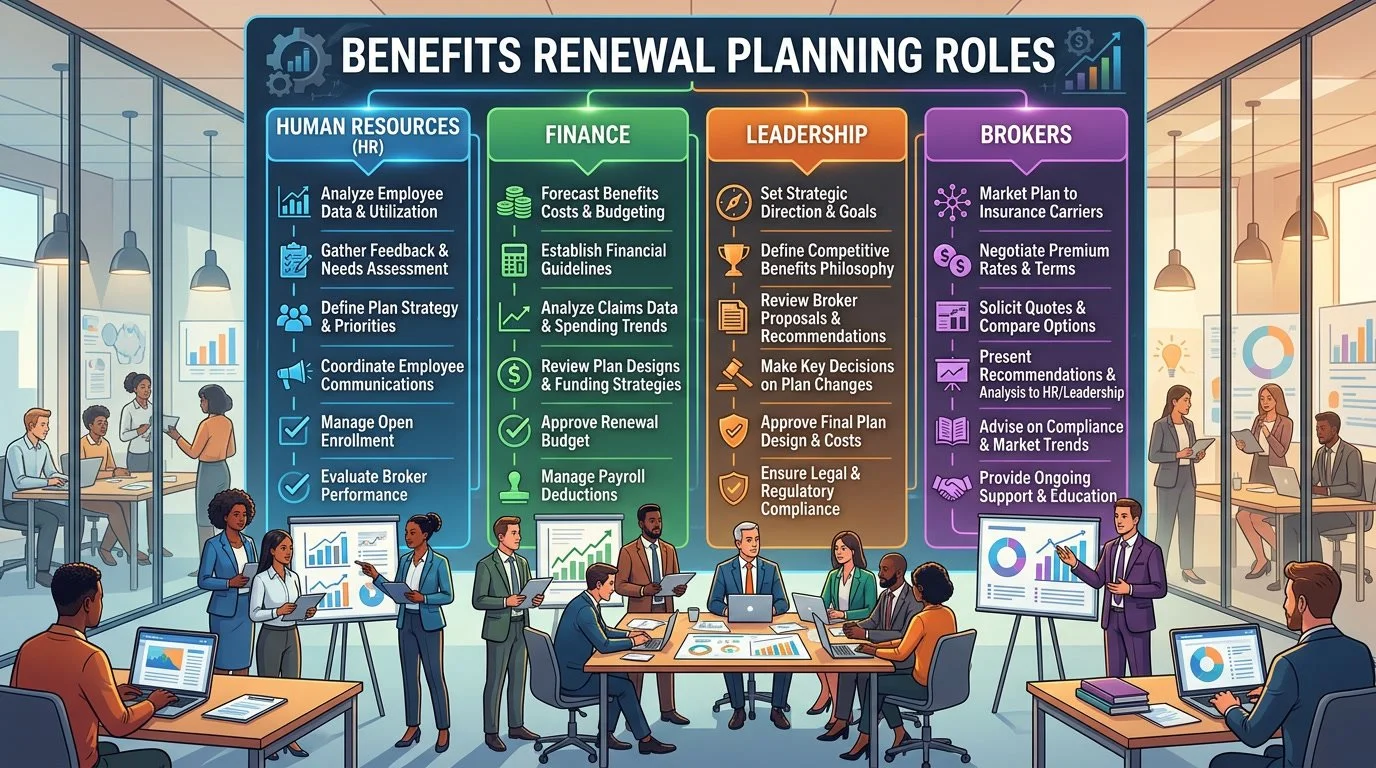

Stakeholder Roles: Who Does What

Renewal success requires clear ownership. Ambiguity about who decides what creates bottlenecks and dropped balls.

Clear stakeholder roles prevent bottlenecks during benefits renewal planning

HR / Benefits Lead

Primary responsibilities:

Owns the renewal calendar and drives timeline adherence

Coordinates stakeholder input and manages broker relationship

Develops plan design alternatives and cost modeling

Leads employee communication and enrollment

Decision authority:

Recommends plan design changes

Manages vendor relationships day-to-day

Approves employee communication content

Finance

Primary responsibilities:

Sets budget parameters and cost constraints

Reviews renewal financials and funding strategies

Approves any benefit changes with budget impact

Decision authority:

Final approval on total benefits spend

Funding mechanism decisions (fully insured vs. self-funded, contribution strategies)

Executive Leadership

Primary responsibilities:

Provides strategic direction on benefits philosophy

Approves significant plan design changes

Champions benefits as part of total rewards messaging

Decision authority:

Final approval on major changes (new benefits, eliminated benefits, significant cost shifts to employees)

Tie-breaker when HR and Finance disagree

Broker / Advisor

Primary responsibilities:

Markets renewal to carriers and negotiates terms

Provides benchmarking data and market intelligence

Supports compliance review and plan documentation

Assists with employee communication and enrollment

Accountability:

Delivers renewal options within agreed timeline

Provides transparent reporting on carrier negotiations

Brings proactive recommendations, not just reactive quotes

Defining these roles upfront prevents the confusion that creates last-minute scrambles. When everyone knows their lane, decisions move faster.

Broker Meeting Prep Checklist

Your broker relationship is a leverage point for renewal success—or a source of dysfunction. Preparation before broker meetings ensures you get value from the relationship and hold your advisor accountable.

Before Any Broker Meeting

Information to gather:

Current enrollment numbers by plan and tier

Claims data (if available and applicable)

Employee feedback on benefits from the past year

Any compliance issues or concerns

Changes to your workforce: growth, new locations, demographic shifts

Strategic priorities for the coming year (hiring plans, retention concerns, M&A activity)

Questions to bring:

What are you seeing in the market for companies like ours?

What renewal increase should we expect based on our experience?

What options exist if the renewal comes in above our budget?

Are there any compliance changes we should prepare for?

What are other clients doing that we should consider?

For the Renewal Marketing Meeting

Documents to request:

Renewal timeline with specific dates

List of carriers being marketed

Summary of plan design alternatives being quoted

Benchmarking data comparing your plans to market

Questions to ask:

How many carriers are you approaching and why those specifically?

What's your strategy for negotiating with our incumbent?

What information do you need from us to get the best quotes?

When will we see preliminary results?

For the Renewal Results Meeting

Information to review beforehand:

Prior year's renewal increase for comparison

Budget parameters established in Phase 3

Alternative scenarios you've already modeled

Questions to ask:

How do these rates compare to what you expected?

What drove the increase (or decrease)?

Where do you see negotiating room?

What would it take to get a better rate with the incumbent?

How do these results compare to market benchmarks?

For Post-Renewal Accountability

Items to document:

Final negotiated rates versus initial renewal

Broker commitments made during the renewal process

Service level expectations for the coming year

Timeline for next year's renewal marketing

Questions to close the loop:

Did we achieve the outcomes you projected?

What should we do differently next year?

What service improvements can we expect from you?

This checklist transforms broker meetings from status updates into strategic conversations. It also creates documentation for evaluating whether your broker relationship is working.

Building Your Renewal Calendar

A framework only works if you implement it. Here's how to translate the 12-month model into an actual calendar.

Step 1: Anchor to your plan year.

Everything flows backward from your renewal date. If your plan year begins January 1, your Phase 4 (execution) runs October through December. Phase 3 (preparation) runs July through September. And so on.

Step 2: Block the key dates now.

Put these on the calendar immediately:

Post-renewal debrief (30 days after enrollment closes)

Mid-year benefits review (6 months before renewal)

Finance budget alignment meeting (4 months before renewal)

Broker renewal kickoff (90 days before renewal)

Leadership decision meeting (45 days before renewal)

Employee communication launch (30 days before enrollment)

Step 3: Assign owners to each milestone.

Every calendar item needs a name attached. Not a department—a person. That person is responsible for making sure the meeting happens and the work gets done.

Step 4: Create a shared tracking document.

A simple spreadsheet works: milestone, owner, due date, status, notes. Review it monthly. Update it as things shift.

Step 5: Protect the calendar from scope creep.

Renewal preparation competes with everything else on your plate. Treat these calendar blocks like external commitments that can't be casually moved.

When Renewal Fatigue Signals a Bigger Problem

Sometimes the chaos isn't just a planning problem—it's a symptom of structural issues that planning alone won't fix.

Signs your situation needs deeper work:

Your broker is reactive, not proactive, year after year

You don't have visibility into what you're actually paying for benefits

Your benefits program hasn't been strategically reviewed in years

You're still on a PEO and wondering if you've outgrown it

Your HRIS and benefits systems don't talk to each other

Leadership treats benefits as a cost center instead of a strategic tool

These situations benefit from stepping back and looking at your benefits infrastructure as a whole—not just optimizing within a broken system. A third-party assessment can identify whether you need a new broker, a different plan design, better technology or a more fundamental restructuring.

The Payoff of Planning

Benefits renewal planning transforms chaos into strategic execution

Organizations that implement a renewal calendar don't just reduce stress—they make better decisions.

With time to gather data, you negotiate from knowledge instead of guesswork. With stakeholder alignment, decisions stick instead of getting relitigated. With documented rationale, you build institutional memory that compounds year over year. With clear communication timelines, employees understand their benefits and use them effectively.

Renewal fatigue is real. It's also optional.

The chaos you experienced last year isn't destiny. It's the predictable result of a system designed for scrambling. Change the system, and you change the outcome.

If renewal season has you bracing for impact, Q Benefits Administration can help. We work with HR and finance leaders to build renewal processes that actually work—planning frameworks, stakeholder alignment, broker accountability and benefits infrastructure that supports your strategy instead of fighting it. Bring us your Q.

Frequently Asked Questions

How far in advance should we start preparing for benefits renewal?

A structured renewal process runs year-round, but active preparation should begin at least six months before your renewal date. This gives adequate time for strategic assessment, budget alignment with finance and scenario planning before underwriting results arrive. Organizations that start 60–90 days out are already behind.

What should I do if our broker isn't proactive during renewal season?

Document specific instances where your broker fell short: missed deadlines, lack of alternatives, no benchmarking data, reactive-only communication. Use this documentation to have a direct conversation about expectations. If patterns continue, consider a broker RFP process to evaluate whether another advisor would better serve your needs.

How do I get leadership to engage with benefits decisions earlier?

Frame benefits in business terms: total compensation competitiveness, retention risk, budget predictability. Provide a one-page renewal brief that summarizes current state, key decisions needed and timeline. Request a single 30-minute meeting at the six-month mark rather than expecting ongoing engagement. Make it easy for them to add value.

What's the most common mistake organizations make during renewal?

Treating renewal as an annual event rather than a continuous process. When all the work compresses into 60–90 days, there's no time for strategic thinking—only damage control. The second most common mistake is not documenting decisions, which means each year starts from scratch without the benefit of institutional learning.

Can we fix renewal chaos without changing our broker or benefits structure?

Often, yes—implementing a renewal calendar and clear stakeholder roles can dramatically reduce chaos even with the same broker and plan design. However, if your broker consistently underperforms or your benefits structure is fundamentally misaligned with your organization, process improvements will only go so far. Sometimes the system itself needs to change.

About Q Benefits Administration

Q Benefits Administration is a benefits infrastructure consulting firm founded by Cora Lynn Alvar, SHRM-CP, who brings over a decade of experience in health and welfare benefits and mid-market consulting. We help HR, finance and operations leaders build benefits programs and processes that reduce chaos and support organizational strategy. When policy placement makes sense for our clients, QBA Insurance Solutions provides that capability—always with transparency about options and client choice. Our project-based approach delivers tangible frameworks, checklists and roadmaps that your team can carry forward long after our engagement ends.

Works Cited

[1] Society for Human Resource Management (SHRM) — "Managing Health Care Costs." https://www.shrm.org/topics-tools/tools/toolkits/managing-health-care-costs

[2] Kaiser Family Foundation — "Employer Health Benefits Survey." https://www.kff.org/health-costs/report/employer-health-benefits-survey/